Meta: A Transformative Social Media and AI Business

Meta: A Transformative Social Media and AI Business

A Deep Dive

***Disclosure: The writer of this report has an investment position in Meta***

***Disclosure: This research report is for academic and entertainment purposes only. None of this should be interpreted as financial advice***

Meta is a mega-corporation that operates social media platforms with billions of daily active people (DAP) worldwide. What makes Meta and most other social media platforms unique is their open platforms that do not directly cost the user money to fully utilize the service. Instead, Meta generates revenue by selling targeted ad placements to third-party advertisers. Instagram and Facebook are Meta's two most valuable assets are part of its Family of Apps segment which generates over $42 billion in operating profit. Similar to other software companies, Meta has a very low cost of revenue as a percentage of total revenue (21.7%). The customer acquisition cost of Meta's social media platforms is virtually nothing due to the nature of software.

Business

Family of Apps

Founded in 2004, Meta's first platform was Facebook, which allows users to connect with each other online, join social groups, and set up pages. In recent years, Facebook has expanded into the e-commerce space with Facebook Marketplace. It is Meta's most profitable business due to several factors. First, Facebook has the oldest user base among Meta's platforms, which naturally comes with greater wealth. Advertisers are attracted to the wealthier user base of Facebook as a means to sell more products at higher prices. The layout of traditional Facebook is also more advertiser-friendly compared to short-form video content formats such as Instagram Reels or TikTok. As with all of Meta's platforms, the most valuable market for Facebook is the United States and Canada region (USCAN). In 2022, almost half of Meta's total revenue came from USCAN, despite the region making up only around ten percent of Meta's users.

Meta acquired Instagram in 2012, a photo-sharing platform targeting a younger audience than Facebook. Over the past decade, Meta has substantially enhanced Instagram's functionality. Meta's Instagram often implements popular social media features from its competitors. In 2016, Instagram unveiled Instagram Stories, a content sharing feature that allows users to temporarily share daily pictures and videos with their followers. This feature was originally made popular by Meta's competitor Snapchat. Meta's most recent major addition in early 2022 is Instagram Reels, a short-form video content platform where users can publish short videos to be seen by anyone. Instagram Reels is designed to compete with its biggest competitor TikTok. This represents a dramatic shift for Instagram from community-centered content to AI-recommended external content.

WhatsApp is Meta's leading messenger app, allowing users in different countries to communicate effectively with each other for free. Unlike Apple's iMessage, WhatsApp allows seamless messaging between any smartphone regardless of the manufacturer or platform. In developed economies outside of the United States, Apple enjoys less dominance, making iMessage less utilized compared to WhatsApp. Effectively, WhatsApp has become the dominant messenger app for Android and non-US smartphone users. Meta has not fully monetized WhatsApp, but there are many paths to full monetization if Meta wishes to pursue it. One of these includes creating a payment platform similar to PayPal’s Venmo. Currently, Meta monetizes WhatsApp through click to WhatsApp ads that allows advertisers to display an ad on Instagram or Facebook that when clicked on opens WhatsApp messages.

Reality Labs

Meta purchased Oculus in 2014, a virtual reality headset assembler. After renaming Oculus to Reality Labs, Meta refocused Reality Labs efforts towards platform building and the metaverse. Reality Labs looks to develop the technology needed to sustain Meta's version of the metaverse, similar to how Apple controls iOS. Meta's most recent consumer headset is the Meta Quest 2, which has sold almost twenty million units as of March 2023. In fall 2022, Reality Labs unveiled its first-ever enterprise-focused headset called the Meta Quest Pro, marketed as a productivity machine. However, with a battery life of just over two hours, the Meta Quest Pro lacks the full capability to replace traditional productivity machines such as laptops. Meta is currently working on next-generation headsets to dominate the hardware and software markets for the metaverse. Meta believes that both software and hardware will generate long-term returns for the metaverse.

Meta Quest Pro

Meta released the Meta Quest Pro in October 2022, a high-end mixed-reality (MR) headset targeting enthusiasts and enterprises priced at $1500. Meta also announced a partnership with Microsoft to deliver immersive experiences for the future of work and play. Microsoft 365 apps will be available on Meta Quest devices, allowing users to access Word, Excel, PowerPoint, Outlook, and Share point within VR. This positions MR as the future of productivity, and Meta as the center of innovation. In March 2023, the price of the Meta Quest Pro was cut by 33% from $1500 to $1000.

Meta Quest 2

The Meta Quest 2 was released in October 2020 at a price of $299 (64GB) and $399 (256GB). Its target audience is the average consumer for recreational use, and it is used to play virtual reality (VR) video games. The price of the Quest 2 has fluctuated but currently sits at $399 and $429 for the 128GB and 256GB models, respectively. Meta has confirmed that the Meta Quest 3 will launch later in 2023.

Financial— Segments

Family of Apps

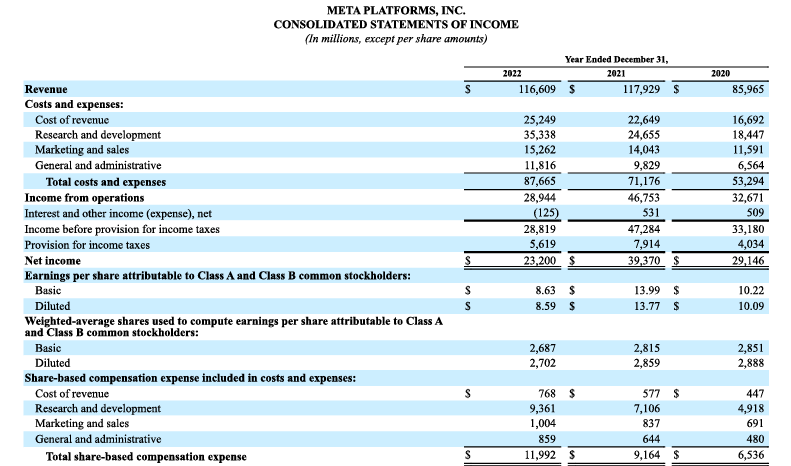

The Family of Apps is Meta's largest segment, accounting for a significant portion of the company's revenue. In 2022, Meta generated $116.6 billion in revenue, of which $114.5 billion was generated through the Family of Apps segment. This segment boasts an impressive 37% operating margin, although operating income declined 25% from $56.9 billion in 2021 to $42.7 billion in 2022. The decline was mainly due to increased headcount expenses, R&D spending, and a softening of the advertising market in 2022, causing expenses to outpace revenue.

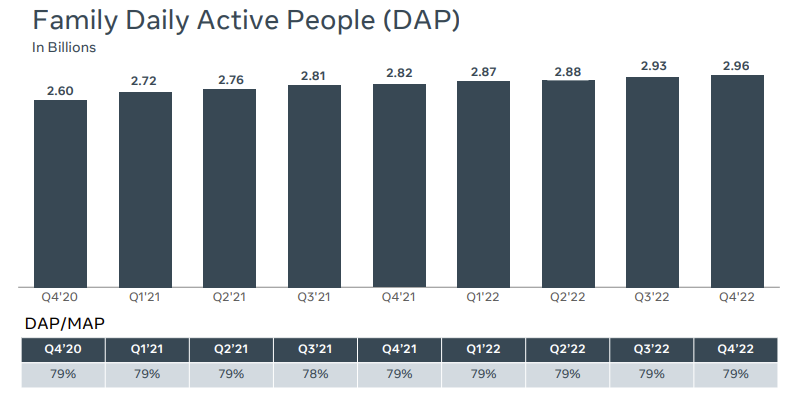

The two primary drivers of the Family of Apps segment are family monthly active people (MAP) and average revenue per person (ARPP). As of Q4 '22, Meta boasts around 3.74 billion monthly active people, a figure that is even more remarkable given that China banned all of Meta's platforms, reducing the potential user base by over one billion people. This highlights the strength of Meta's reach, which is undeniably stronger than any of its competitors. However, limited growth potential exists for MAP.

ARPP provides more nuanced insight into Meta's performance. It is much more likely to grow for a variety of reasons, including increasing ad rates, increasing ad impressions per minute, and increasing time spent on platform. As GDP rises in developing economies, discretionary income will rise faster than disposable income, resulting in a disproportionate increase in ad rates for the majority of Meta's users. Ad rates can also increase as a result of better ad targeting from Meta's new AI investments. Ad placements are another area where Meta could potentially increase its revenue. However, an increase in ad density could hurt user engagement, leading to reluctance to significantly increase ad density.

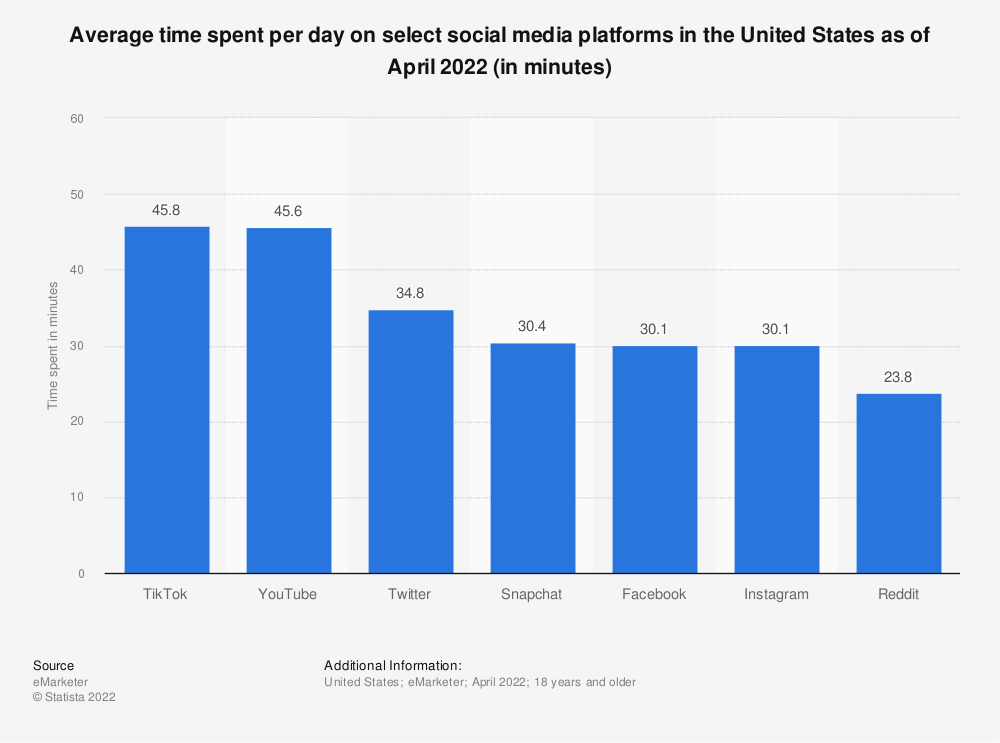

An increase of time spent on platform seems to be one of the more likely candidates for ARPP growth due to one main underlying factor. The increase in prevalence of Instagram Reels, like most other effective short form content platforms, increases time spent on the platform substantially. According to Statista, in April 2022, Tik Tok users on average spent about 46 minutes per day on the app. Instagram and Facebook both sat at 30 minutes, respectively. This represents a potential 50% increase in time spent on platform if Meta is able to reach parity with Tik Tok and YouTube.

Meta has been investing billions of dollars into building its server infrastructure to store vast amounts of data and host its new AI powered algorithms. Meta is looking to create the most engaging short form video platform in the world. While Meta most recently announced that it will reduce its planned server spend, Meta’s new server spend will still be substantial.

Reels Monetization

At the present, Reels poses a headwind for Meta's advertising revenue due to its lower advertising run rates in comparison to other ad placement spots such as Feed or Stories. However, by 2024, Reels is anticipated to become a net tailwind and make a positive contribution to Meta's revenue. In 2022, Reels generated a run rate of $3 billion, but it is expected that Reels' revenue will increase significantly as its monetization rates align more closely with those of Feed and Stories.

AI Driven Advertising

Meta has disclosed that advertisers who used Advantage+ shopping campaigns experienced an average increase of 32% in their ROAS, while more broadly, advertisers saw a 20% increase in conversions compared to the previous year. This increased ROAS allows Meta to charge higher rates for its ad space. The effectiveness of advertisers is largely due to their investments in AI, which demonstrates the efficacy of Meta's investment strategy. Additionally, Meta's new ad tools leverage AI automation, making it easier for advertisers to market their products and services on Meta's platforms. The AI automates the targeting process, optimizing ad spend to achieve specific goals, thereby freeing advertisers from having to handle the targeting themselves.

Reality Labs

Reality Labs continues to lose money for Meta. In 2021, Reality reported an operating loss of over $10.1 billion. In 2022, the company reported that the operating losses grew by over 30% to an operating loss of $13.7 billion. Reality labs is not projected to have a positive return in the next few years and will likely incur similar losses in the future. This is a result of several factors including:

High R&D expenses as a result of salaries

Selling hardware at a loss

Lower than expected demand

Year of Efficiency

During the Q4 2022 earnings call, senior management expressed a new priority that Meta would be pursuing throughout 2023. Mark Zuckerberg emphasized that 2023 would be a year of efficiency for Meta, and he explicitly noted some of the measures the company would be taking are as follows

Meta plans to deliver its roadmap by working closely with its infrastructure team, while reducing its planned capital expenditures (data centers and network infrastructure).

To expedite decision-making, Meta will "flatten" its organizational structure by eliminating middle management positions.

Managers at Meta will have fewer than ten direct reports.

Meta intends to improve engineering productivity by deploying artificial intelligence (AI) tools.

Meta will proactively cut projects that are underperforming or no longer considered crucial.

Most importantly, Zuckerberg emphasized the importance of increasing Meta's efficiency in executing its top priorities, which are AI and the metaverse. In particular, he focused on the AI discovery engine that drives content discovery on Facebook and Instagram.

Susan Li, the CFO, estimated that total expenses would be in the range of $86-92 billion, lowered from the previous outlook of $89-95 billion. Li expects capital expenditures to be in the range of $30-33 billion, lowered from the previous estimate of $35-37 billion. This decline is due to a reduction in expected data center spend in 2023.

Restructuring

During 2022, Meta announced the layoff of more than 11,000 employees. In addition to the layoffs, Meta announced that it would be restructuring parts of the company. The Restructuring charges amounted to around $4.6 billion and are not recurring. The cause of these charges are as follows:

Facilities restructuring

Layoff of 11,000 employees

A pivot towards next gen data center design, including cancellation of multiple projects

Legal

Meta has been involved in a series of legal and regulatory battles with various entities for years. These battles have pitted Meta against various entities from other corporations and users to governments. In particular, Meta has a tumultuous relationship with the EU who regularly hits the social media giant with fines and lawsuits. More recently, the EU has taken aim at Meta’s transatlantic data transfers from the EU to the US. Regulators are trying to restrict companies like Meta from migrating data from the EU to the US. Going forward, it is likely regulatory battles continue to plague Meta.

Financial Statements

Balance Sheet

Ratios:

Current Ratio: 2.2

Debt to Equity Ratio: .48

Meta possesses one of the most pristine balance sheets on the entire market. With a current ratio of 2.2 (down from 3.15) and a debt to equity ratio of .48, the chance of bankruptcy or insolvency in the foreseeable future is virtually nonexistent.

Meta’s two most noticeable changes are PPE and Debt. Over the last two years, Meta has drastically increased its investment in servers and network assets to support an increase in its AI workloads. Servers and network assets make up over half of gross property and equipment when assets under construction are taken into account. This marks a fundamental shift in Meta’s fixed asset requirements. As a result, moving forward, capital expenditures are expected to remain substantially elevated when compared to 2020 levels.

The second major change is the debt levels. Prior to 2022, Meta had financed none of its operations through the issuance of long-term debt. In August of 2022, Meta issued $10 billion in debt with maturity dates ranging from 2027-2062. Meta’s debt creates $411 million in interest payments in 2023. It is not uncommon for sustainable unlevered companies to issue debt to get the benefits of tax deductible interest expenses in conjunction with an inflow of cash.

In February of 2023, Meta announced a stock buyback of $40 billion. Because the company has a low bankruptcy risk, Meta was able to issue debt at a low interest rate and buyback shares with a substantially higher yield.

Income Statement

Gross Profit Margin: 78%

Operating Margin: 24.8%

Net Margin 19.9%

In 2022, Meta faced significant challenges, particularly evident in its income statement. Despite generating revenue of $117.9 billion in 2021, Meta's revenue decreased slightly to $116.6 billion in 2022. This decline was mainly due to a 16% decrease in the average price per ad in 2022 compared to 2021, resulting from an increase in ads delivered at lower ad monetization rates and to platforms that fetch lower prices per ad such as Reels, as well as economic uncertainty. However, the revenue decline was partially offset by an 18% increase in ads delivered in 2022 compared to 2021.

Meta also struggled with costs in 2022, with Cost of Revenue as a percentage of revenue increasing from 19% to 22%, primarily due to increased operational expenses related to data centers. Research and development as a percentage of revenue also increased from 21% to 30% in 2022 due to a 26% increase in employee headcount in engineering and technical functions. General and administrative expenses increased by 20%, primarily due to a 20% increase in payroll expenses.

In response to these challenges, Meta committed to laying off at least 21,000 employees, representing about 25% of the total employees. However, increased costs and decreased revenue significantly impacted Meta's profitability, with operating margin declining from 40% in 2021 to 25% in 2022. Meta's Family of Apps operating profit declined 25% from $56.9 billion to $42.6 billion in 2022, and Reality Labs operating profit declined 35%, representing a $13.7 billion loss in 2022. Meta's profitability remains a significant concern.

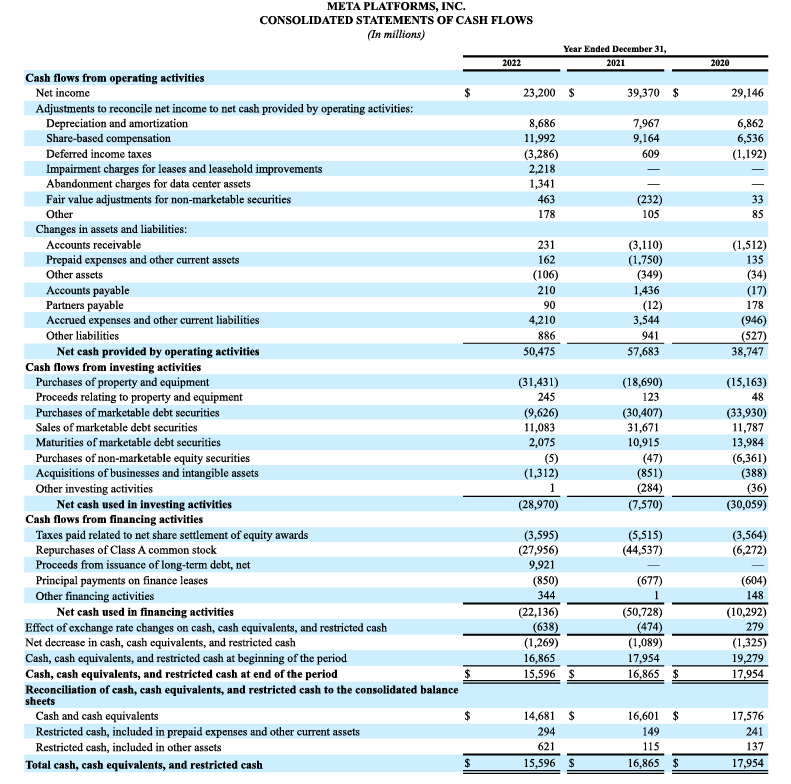

Statement of Cash Flows

Meta's cash flow has emerged as a significant concern for the company. In 2022, free cash flow declined by 51%, which was primarily due to a 13% decrease in cash flow from operating activities and a 68% increase in capital expenditures. The rise in capital expenditures can be attributed to the company's intense focus on investing in data centers and servers to drive AI development. According to Meta, 86% of capital expenditures go towards supporting the Family of Apps business. Going forward, it is expected that the composition of capital expenditures will shift even further towards data center and server investment.

Competitors:

TikTok

TikTok is the closest peer to Meta in the social media industry, with over a billion monthly active users worldwide. TikTok pioneered algorithm-based content with its short-form video "For You" page that suggests content based on what it believes the user enjoys. TikTok's biggest advantage is its Gen Z dominance in the United States. According to Pew Research, 67% of teens (13-17) use TikTok compared to 62% for Instagram. In this study, Facebook went from 71% in 2014-2015 to 32% in 2022, showing a drastic drop in usage rates. TikTok also seems to be more engaging, as 16% of teens say that they are “almost constantly” on TikTok compared to only 10% for Instagram and 2% for Facebook.

TikTok’s Uncertainty

In recent years, TikTok has come under political pressure. TikTok's parent company, Bytedance, is based in China, causing some lawmakers to worry about potential national security risks. In June 2020, TikTok was banned in India over security concerns, resulting in a loss of approximately 200 million users. In 2020, President Donald Trump attempted to ban the app but was blocked by the courts. In response, TikTok moved all of its US user data over to Oracle's data centers located in the United States. In March of 2023, Congress subpoenaed the CEO of TikTok, Shou Zi Chew. He was grilled for hours, and the message was clear: a Chinese-affiliated TikTok is not allowed in the US. It is likely that the US will force a spinoff of the famous social media app. However, this spin-off may stall TikTok's ability to operate.

Alphabet (Google)

Google is the largest player in the digital advertising space, with over $224.5 billion in revenue in 2022. This is almost twice the amount of digital ad revenue that Meta generated in the same year. Google offers advertising in a few different ways. The first and largest is Google Search, which allows advertisers to display their ads on Google search result pages. The second-largest advertising service is the Google Network, which allows websites to opt into an advertising program where Google pays them based on performance metrics such as views and clicks in exchange for advertising space. The final digital advertising platform is YouTube ads. YouTube is a video platform where creators can share long-form video content and livestreams. YouTube is the closest peer to Instagram and Facebook that Google has and is at the greatest risk of overlap. As companies become more conscious about their ad spend, much of Meta’s potential growth could be consumed by other large digital advertising giants such as Google and Amazon.

Amazon

Amazon is a new major player in the digital advertising space. In 2022, advertising services grew by 21.1% to $37.7 billion. Amazon's advertising services allow advertisers to market directly on an ecommerce platform. Amazon's advertising service inherently possesses two advantages that Meta does not. Firstly, Amazon knows exactly what its customers are looking for through its product search. Secondly, Amazon has a recorded history of customers' past purchases. When these two factors are combined, Amazon can offer an advertising service that is unrivaled.

Conclusion

In conclusion, Meta is a robust business with multiple sustainable revenue sources. However, questions remain regarding the company's ability to maintain its competitive edge in the fast-paced social media and digital advertising industries, as well as the effectiveness of its investments in areas like Reality Labs. Nevertheless, Meta's unparalleled scale and reach set it apart from other players in the social media space. Despite a significant compression in margins since 2021, Meta's unwavering focus on server and AI infrastructure ensures that the company will continue to leverage cutting-edge technology and stay ahead of the competition as it aims to retain its dominant position in the industry.