Intel Deep Dive: A Misunderstood Business

Intel Deep Dive: A Misunderstood Business

By Ben Rossi

**Disclaimer: This post is for educational and entertainment purposes only. This report should NOT be misconstrued as financial advice**

Executive Summary

Intel Corporation (INTC)

Intel Corporation is one of the largest semiconductor companies in the world. Intel is an integrated device manufacturer (IDM). As a result, Intel designs and manufactures its own chips.

In recent years, Intel has struggled with innovation. Competitors such as TSMC, AMD, and Nvidia have chipped away at Intel’s market share. The previous CEO, Bob Swan, failed to foster a culture of innovation vital to operating in the semiconductor industry. After being replaced in 2021, Bob Swan’s successor, Pat Gelsinger immediately shifted the company’s focus towards IDM 2.0, focusing on technology and manufacturing capacity. This initiative comes at significant capital costs partially offset by Western nations’ subsidies in the aftermath of global COVID-19 supply chain disruptions.

While risks remain within the plan, IDM 2.0 creates a unique value proposition for potential clients. First, Intel’s current node roadmap is technologically superior to its main competitor, TSMC. Furthermore, Intel will have a geographic monopoly on advanced semiconductor nodes. TSMC’s announced expansions in the United States will no longer be generations behind Intel’s at the estimated time of release.

As a result of these factors, Intel trades at a discount to its Intrinsic value. The market and intrinsic value gap exists due to poor short-term business performance and execution risk. Our three-statement DCF model suggests a target share price of $71.44.

Table of contents

Introduction

History

Management

Top Executives

Capital Allocation

Business

Industry

Business Model

Segments

Technology

Financials

Income Statement

Balance Sheet

Statement of Cash Flows

Financial Statement Analysis

Competition

Competition Overview

Valuation

Assumptions

Model

Conclusion

Introduction

Intel is one of the world’s largest semiconductor companies. Intel primarily constructs central processing units (CPUs) that function as the computer's brain. These parts are predominately sold to system builders such as Hewlett-Packard (HP) and Dell. In addition to system builders, CPUs are sold to larger corporations for data centers and high-performance computing (HPC). Recently, Intel has shifted its focus towards IDM 2.0, selling parts of Intel’s manufacturing capacity to third parties. In addition to IDM 2.0, Intel has moved into parallel niches such as graphics processing units (GPUs) and AI accelerators.

History

Intel was founded on July 18, 1968, by semiconductor legends Gordon Moore, Robert Noyce, and later Andy Grove. Gordon Moore and Robert Noyce had previously worked for the semiconductor company Fairchild Semiconductors but left after R&D was adversely impacted by Fairchild Semiconductor’s parent company. In 1971, Intel introduced the world’s first electronically programmable microprocessor. Intel continued to lead the semiconductor industry up until the mid-2010s. From 2016 to 2022, Intel struggled to innovate from its 14nm manufacturing process to its 10nm manufacturing process. These delays led to TSMC and Samsung overtaking Intel in the technology race. These delays also sparked major industry shifts that allowed for increased competition from companies such as AMD and Apple.

In 2020, Apple announced it would shift away from using Intel processors in its desktop and laptop platforms. Apple introduced Apple silicon for its platforms, incorporating TSMC manufacturing to create these chips. The technology gap between TSMC and Intel also allows AMD to leap over Intel in consumer and enterprise CPUs. In many cases, Intel has been forced to use 3rd party manufacturing to stay competitive with the rest of the industry.

Management

Top Executives

CEO: Pat Gelsinger

Since: February 2021

Pat Gelsinger started his career in 1979 at Intel. He became the first chief technology officer (CTO) in Intel’s history. Gelsinger left Intel in 2009 to join EMC as president and COO. In 2012, Pat Gelsinger became CEO of VMware, tripling its profits from 2012 to 2021. In 2021, Gelsinger succeeded Bob Swan as Intel's CEO amidst the company's technological deterioration. Gelsinger is viewed as a leader of innovation and focuses heavily on core technologies. In 2021, Gelsinger unveiled IDM 2.0, a strategy designed to rejuvenate Intel’s deteriorating business.

CFO: David Zinsner

Since: January 2022

David Zinsner is executive vice president and chief financial officer (CFO) at Intel. Before joining Intel, Zinsner served as Micron’s chief financial officer. Zinsner has substantial experience managing the finances of several technology companies. Following Swan’s exit from Intel. Gelsinger and the board made several major changes to the C-suite. Zinsner is a crucial part of this reformation.

Capital Allocation

Intel’s shift to IDM 2.0 has transformed the company from a moderately capital-intensive business to a highly capital-intensive business. Intel is taking advantage of the US CHIPS Act and the upcoming EU CHIPS Act to build a diverse supply chain for its manufacturing. Intel is estimated to receive anywhere from $15 to $17.5 billion in subsidies and loans from the US CHIPS Act. The details regarding the EU CHIPS Act are still being worked on, but Intel is expected to be a prominent benefactor of that bill.

In early 2023, Intel announced it would cut its quarterly dividend by 66% to 12.5 cents. Intel’s dividend cut shores up over $3 billion in cash annually. The reduction of the dividend aligns with IDM 2.0’s capital allocation strategy.

Under Gelsinger, Intel has focused on refining its business. As of July 27th, 2023, Intel has exited nine businesses, saving $1.7 billion annually. There is a noticeable move towards more concentrated objectives, including manufacturing process technology and capacity, AI accelerator products, GPUs, and CPUs.

The geographical nature of Intel’s investments is crucial to the success of Intel’s foundry business. COVID-19 supply chain disruptions illustrated the flaws of a heavily-concentrated semiconductor manufacturing industry. Taiwan makes up the majority of advanced semiconductor manufacturing. Intel’s focus on manufacturing in developed markets such as the US and EU creates a more robust supply chain for clients. In addition a to more robust supply chain, Intel has been able to take advantage of subsidies.

Business

Industry

The Semiconductor industry comprises several different types of businesses that operate to create today's technology-driven world. Equipment manufacturers supply foundries with the equipment that allows foundries to create fabs. Foundries then sell their fabs’ manufacturing capacities to fabless design companies to produce the designs. These designs include more mainstream products such as AMD and Nvidia processors. Once the Foundries produce the fabless design companies’ designs, they are sent to assembly, testing, and packaging to be readied for sale.

Business Model

Intel is an integrated device manufacturer (IDM) primarily producing x86 CPU designs and microprocessors. This means it acts as a foundry and a fabless design company. Intel historically designs and manufactures its chips. In 2021, Intel pivoted towards a foundry business to complement its IDM business. Intel calls this strategy IDM 2.0.

As an IDM, Intel both designs and manufactures its products. In recent years, Intel has acted as both a fabless design company and a foundry. For example, Intel launched GPUs in 2022. These GPUs were designed by Intel but produced by TSMC (a foundry). In contrast, Intel has been looking for clients to sell its fab capacity to since Pat Gelsinger’s appointment. Intel’s current cost per wafer, a measure of how cheaply Intel can produce semiconductors, is roughly 50% higher than TSMC’s. As Intel scales its manufacturing, this cost will decrease. However, the use of higher-labor cost manufacturing countries such as the United States and Germany will continue to cause elevated costs for Intel.

Intel’s products are intermediate goods that are used to build computers. Intel’s most prominent product is the central processing unit (CPU). CPUs are essentially the brains of the computer and drive the majority of a computer's performance. CPUs are predominately used in consumer and professional computers, servers, data centers, and supercomputers. Intel has a strong foothold in all the listed markets. However, the CPU market has become increasingly competitive since the launch of AMD’s Zen architecture. Additionally, graphics processing units (GPU) and data processing units (DPU) have represented a substantial threat to the historical dominance of CPUs in supercomputers.

Segments

Client Computing (CCG)

The Client Computing Group consists of processor sales to original equipment manufacturers (OEMs) and retail sales. Intel has strong relationships with major OEMs such as Dell and HP. Intel sells CPUs and GPUs to OEMs to put in PCs as well as to consumers through merchants such as Newegg. Some of these products include Intel’s Core series CPUs and Intel Arc GPUs. CCG is Intel’s most significant revenue segment.

Data Center and AI (DCAI)

The Data Center and AI segment sells processors to organizations for enterprise servers, data centers, and supercomputers. These products include Intel’s Xeon series CPUs as well as Intel’s Gaudi and field programmable gate array products (FPGA). DCAI makes up the second-largest revenue segment for Intel. Gaudi 2 is Intel’s premier AI accelerator and performs in line with Nvidia’s last-generation A100 processor. Intel plans to release the Gaudi 3 AI accelerator in early 2024, looking to compete with Nvidia’s top-of-the-line H100.

Network and Edge (NEX)

The Network and Edge segment comprises several different networking solutions. Intel offers several ethernet, 5G, and other connectivity products. These products are necessary to support the ever-increasing connectivity in the world.

Mobileye

Mobileye is a publicly traded advanced driver assistance systems (ADAS) and autonomous driving company. Mobileye builds the software and hardware necessary to facilitate ADAS and autonomous driving. Mobileye supplies software and hardware to many major automobile makers, including Volkswagon, Ford, and BMW.

Intel Foundry Services (IFS)

The Intel Foundry Services segment consists of a 3rd party manufacturing business that creates chips for fabless design companies. This business is the focal point of IDM 2.0 and among the most promising segments for Intel. Intel has been building fabs worldwide to accommodate this business and has utilized the unstable supply-chain environment to secure billions in subsidies.

Technology

When Pat Gelsinger became CEO in 2021, Intel’s priorities shifted toward manufacturing capabilities. Intel released a roadmap for five new process nodes, with the final one releasing in 2024. After some delays and releases, the current roadmap has four nodes releasing through 2025, with them being:

Intel 4 (H2 2023)

Intel 3 (H1 2024)

Intel 20A (H2 2024)

Intel 18A (H1 2025)

Among the nodes above, Intel 3 and Intel 18A are the most commercially promising. These nodes are said to be full nodes, meaning they have all the necessary components to make an entire chip. This means that Intel 3 and Intel 18A will be the nodes on which fabless semiconductor design companies manufacture chips. In contrast, Intel 4 and Intel 20A are partial nodes containing only some of the components to build a full chip. These node processes will be the stepping stones to creating complete Intel 3 and Intel 18A nodes for full use. From Intel 7 (the current node) to Intel 18A, Intel’s performance per watt (PPW) is expected to increase by roughly 80%. It will be the PPW leader when Intel 18A releases in early 2025. Intel’s largest competitor, TSMC, will release its N2 process shortly following. However, based on TSMC’s estimates for N2, Intel’s 18A process will be more efficient and offer better performance.

Financials

Income Statement

Intel’s Income Statement paints a bleak picture for the company. Revenue for the full year 2022 is down 20% yoy. Despite the decrease in revenue, Intel’s cost of sales has risen 3% yoy. These two figures culminate in 2022 gross profit decreasing 39% yoy. Operating profit margin went from $19.5 billion in 2021 to $2.3 billion in 2022, representing margins of 25% and 4%, respectively. The first two quarters proved to be an even bigger debacle. Intel’s H1’23 revenue decreased 27% yoy. Intel’s quarterly loss was the largest in the company’s history.

The biggest takeaway from Intel’s income statement is the eroding competitive position of the firm. Intel has long been able to mask its wasteful investment and technological delays in its high margins and ROIC. However, today’s Intel lacks the competitive advantage that it held even six years ago. As competition increases in the CPU consumer and data center markets, Intel is forced to compete on price. Every cent discounted from an Intel processor disproportionately lowers the gross profit margin.

Balance Sheet

Intel’s balance sheet raises several short-term concerns that must be considered. While the current assets are an impressive $43 billion, Intel’s IDM 2.0 strategy is heavily concentrated around capital investment. For example, Intel’s Ohio fabs are estimated to cost $20 billion. Intel’s Arizona fab complex will cost between $60 and $120 billion. Furthermore, Intel’s Germany fab and Israel fab will cost an additional $50 billion combined. In short, there is a need for more cash in order to execute IDM 2.0. Over the next few years, it is safe to assume that debt will moderately increase if Intel cannot generate sufficient cash flows.

Statement of Cash Flows

Intel’s statement of cash flows demonstrates the underlying business shifts in numbers. First, Intel’s cash flow from operations has decreased by 56% to $15 billion from 2020 to 2022. The decreased operating cash flow demonstrates the elimination of Intel’s technological advantage. The second notable change on the cash flow statement is the increase in capital expenditures by $10 billion or 74% to $25 billion over the last two years. Intel’s operating cash flows were negative yoy, decreasing by over 100%. Intel’s capital expenditures increased 12% yoy for the H1’23. This increase is driven predominately by Intel’s IDM 2.0 fab expansion projects. These should be interpreted as growth capital expenditures as they will drive further growth for the business.

Financial Statement Analysis

Intel’s financial statements are poor. The decline in revenue, net income, and free cash flow is concerning. In addition to these declines, the balance sheet is also experiencing substantial degradation.

At the earliest, the IDM 2.0 strategy will not help Intel see any substantial financial improvement until 2025. Investors should pay special attention to Intel’s increasing debt load. More importantly, investors should monitor the pace at which Intel achieves its technological roadmap. Intel's financials will lag behind the business's underlying fundamentals during times of change. During Bob Swan’s tenure, Intel’s financials were spectacular. However, the underlying technological position of Intel was deteriorating, leading the financials to follow.

Competition

Competitive Overview

As an IDM, Intel mainly competes with:

Foundries

TSMC

UMC

Global Foundries

Fabless Design

AMD

Nvidia

Qualcomm

Apple

IDMs

Samsung

Texas Instruments

Intel’s competitive environment varies substantially from segment to segment. Furthermore, performance can vary in different spaces of the same segment. For example, Intel’s CPU design team competes in a stable position relative to its GPU design team despite both being design components. Intel’s fab business progress can also hamper or enhance the design teams. For example, Intel’s fab business failed to shift from its 14nm process to its 10nm process from 2016 to 2022, hindering the CPU design team.

TSMC is the world leader in advanced manufacturing processes and capacity within the foundry industry. TSMC’s most advanced node, N3, is currently in production, with plans for the N2 node to be released in 2025. Taiwan produces 60% of the total global semiconductor supply. Taiwan’s TSMC also produces 90% of the world’s advanced semiconductors. With the introduction of Intel’s future nodes and increased capacity, TSMC’s share of advanced semiconductors will likely decline.

Intel’s design teams compete with AMD and Nvidia within the processor and accelerator markets. Intel’s focus is predominately on CPUs, GPUs, and AI accelerators. Nvidia is the strongest competitor within the AI accelerators and GPU space. Nvidia’s premier offering is the H100 AI accelerator. AMD is Intel’s strongest competitor in the CPU space. AMD’s main offerings in the CPU space are the Ryzen and EPYC processors.

From the graph shown above, we can see that the data center x86 market share is narrowing between Intel and AMD. This is primarily due to the core density and energy efficiency delivered by AMD EPYC series processors when compared with Intel’s Xeon processors. The top of the line EPYC 9754 has 128 cores compared with 60 cores on the Xeon Platinum 8490H.

The graph above shows the geometric mean of a series of enterprise data center CPU benchmarks. AMD wipes the floor with Intel on performance with its new EPYC series processors. The top-of-the-line Xeon Platinum 8490H offers roughly half of AMD’s EPYC 9754 performance.

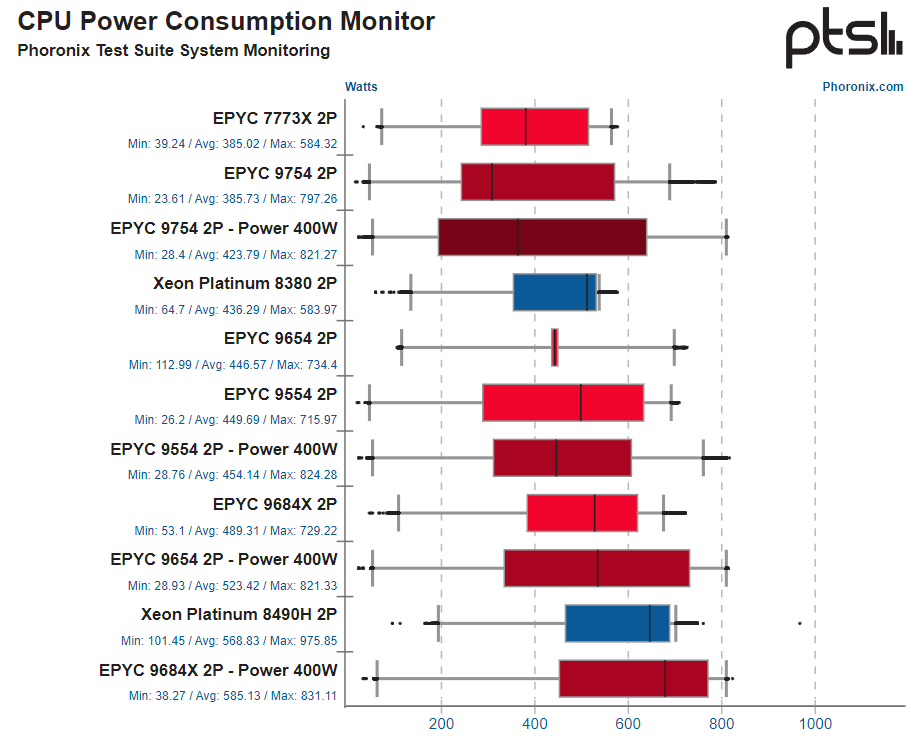

The graph above shows the average power consumption of the CPUs during the previous tests. Despite offering roughly half the performance of AMD’s Xeon Platinum 8490H top offering, Intel consumes more power on average.

Pat Gelsinger recently commented on Intel’s position in the enterprise data center market. He said that Intel has not been competitive, but the upcoming release of Granite Rapids 6th generation Xeon early next year will change the competitive landscape of the enterprise CPU landscape. These processors will be built on the Intel 3 process and have roughly twice as efficient as the current lineup of Xeons. However, Sierra Forest marks the true shift in the Xeon lineup. First, these CPUs will have up to 144 energy-efficient cores on the Intel 3 process. These CPUs will be over 2.4 times more efficient than current Xeons and have more cores than AMD’s current enterprise data center CPU lineup. These cores will also be E cores designed for efficiency. This is a direct competitor to ARM-based CPUs with high core counts and efficiency. AMD has no revealed plans for efficiency-core data center CPUs.

Intel’s market share in the consumer PC market has held up substantially better than the enterprise data center market. This is primarily due to strong OEM relationships and a lesser emphasis on efficiency (most consumers do not care about personal power consumption). In addition to these factors, Intel and AMD remain competitive with each other at all price points of this market. Unlike data center CPUs, the impact of core constraints in the PC market is much lower because consumer CPUs max out at around 20-30 cores.

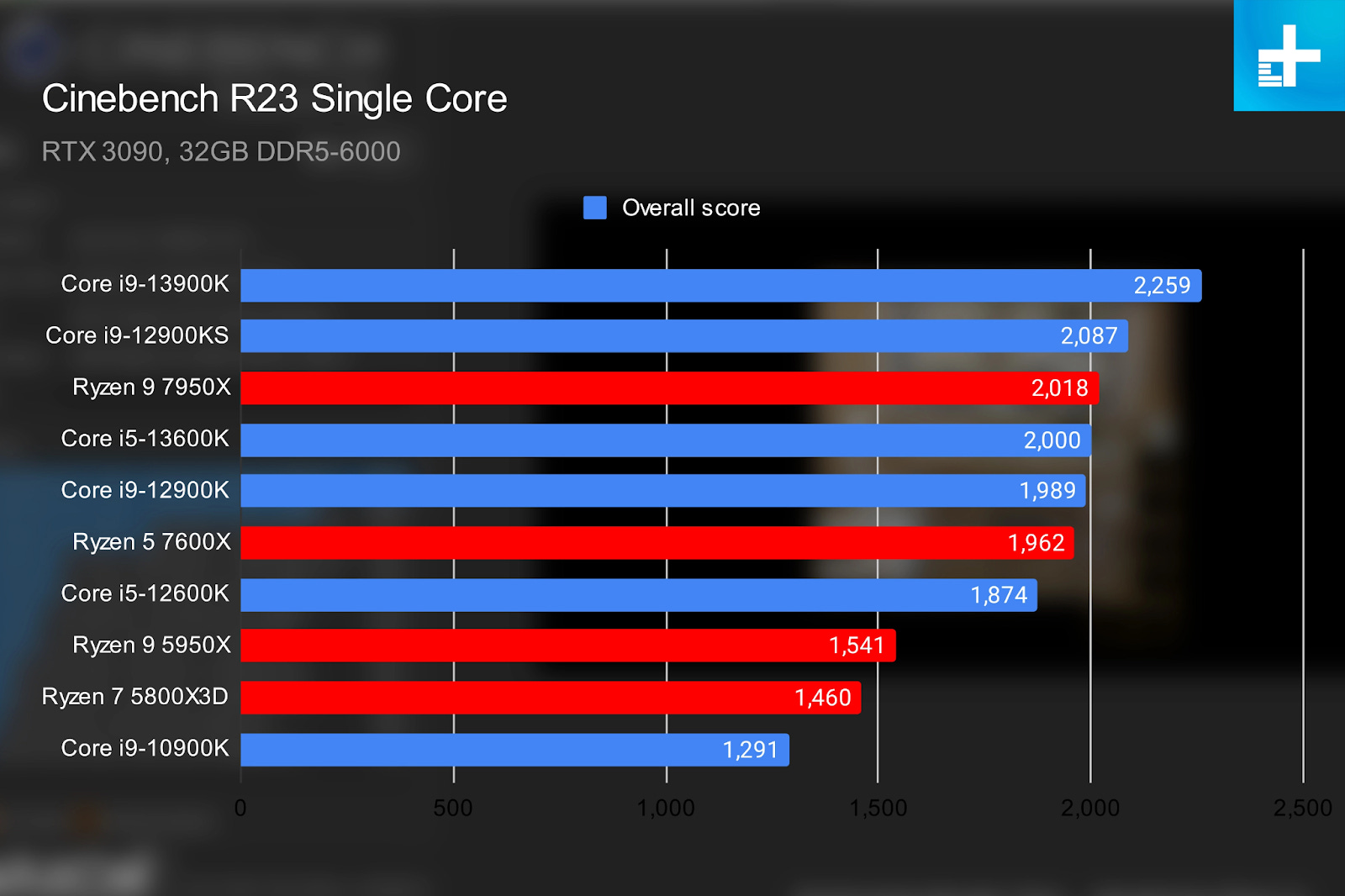

Source: digitaltrends.com

The Cinbench R23 Single-Core test is used to measure the strength of a single core in a CPU. Single-core performance is most important in gaming tasks where higher clockspeeds drive better performance. Intel’s 13900K performs marginally better than AMD’s Ryzen 9 7950X. Additionally, Intel’s mid-line 13600K performance is marginally better than that of the Ryzen 5 7600X.

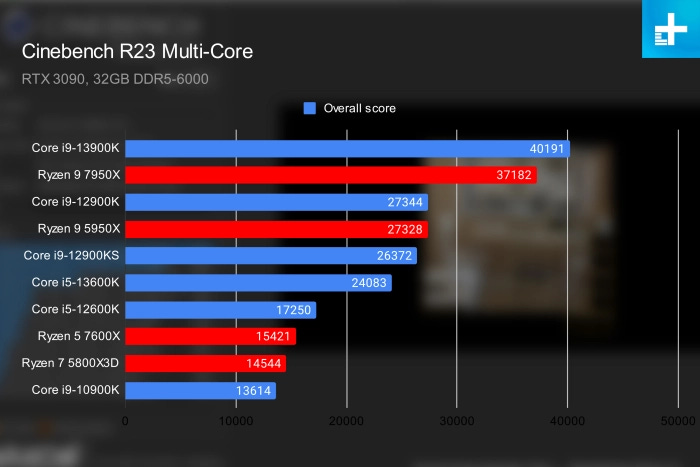

Source: Digitaltrends.com

The Cinebench R23 Multi-Core test is used to measure the performance of all of the individual cores utilized together. CPUs with better multi-core scores are typically able to handle productivity tasks better. Intel outperforms AMD across the board in multi-core tasks regardless of price point. This is reflected in Intel’s increasing market share since late 2022.

Valuation Model

Conclusion

Intel’s business has changed substantially over the past few years. While Intel is no longer the clear market leader in the CPU space, its transition towards manufacturing capacity creates a lot of opportunity. Unlike TSMC, all of Intel’s fabs are located in the West, creating a unique customer value proposition. In addition to Western-based manufacturing, Intel has a roadmap to surpass TSMC’s node process technology. Despite a promising outlook, many risks remain, such as debt and execution, that investors should take into account. Our analysis suggests that Intel is undervalued, with a target share price of $71.44.