Bad Managements Destroy Great Companies

Bad Managements Destroy Great Companies

The Tragic Tale of Intel

Flashback to August 2015, and Intel was sitting at the top of the microprocessor world. The company had just released the Skylake microarchitecture processors, boasting the most advanced manufacturing processes. Intel’s Core processors dominated the consumer PC market, while its Xeon processors had all but consumed the enterprise market. Meanwhile, long-time competitor AMD was still selling Bulldozer-based processors that were less efficient and less powerful than even the lowest-end Intel Core processors. So, what’s changed since then?

Introduction to Management

A publicly traded corporation’s management should ultimately have one prime objective: to increase shareholder value. Management can do this in a multitude of ways, including investing in projects that will yield a return above the cost of capital, buying back common shares at a price below intrinsic value, divesting in segments that return below the cost of capital, issuing dividends to recognize hidden shareholder value, making acquisitions, and more. Intel used all of these strategies in an attempt to increase shareholder value.

A Very Brief History of Intel’s Recent CEOs

In 2013, Brian Krzanich became the CEO of Intel. Krzanich had been with Intel since 1982 and started off as an engineer. Krzanich invested heavily in the research and production of Intel’s fab technology. Krzanich presided as CEO of Intel during its golden years, starting with Haswell in 2013 and ending with Coffee Lake in 2018.

Bob Swan became interim CEO immediately following Krzanich’s departure. Swan ascended to CEO in January 2019. Bob Swan served as eBay’s CFO from 2006 to 2015 before becoming the CFO of Intel in 2016. Swan had no background in engineering but was undoubtedly an effective CFO for both eBay and Intel. Swan’s decisions as Intel CEO will be further discussed in this article. Swan was removed from CEO in early 2021.

Patrick Gelsinger started at Intel in 1979, becoming Intel’s first Chief Technology Officer in 2000. Gelsinger left Intel in 2005 and served as an executive at many other companies before returning to Intel in 2021 to serve as CEO. Gelsinger is the current CEO of Intel and is focused on restoring the competitive position of Intel in the microprocessor space.

Changes in Competitive Environment

With some of the background out of the way, it is important to discuss exactly what went wrong from the beginning.

During Krzanich’s tenure, Intel began developing its 10nm manufacturing process to replace its 14nm Skylake microarchitecture. Unfortunately for Intel, delays were frequent. At the time, Intel had no competitors, so management did not take much notice. Behind the scenes, however, AMD and TSMC were developing products that could rival Intel’s. In 2017, AMD released the Ryzen processors based on the new Zen microarchitecture. AMD’s Ryzen processors were cheaper and offered more cores than their Intel counterparts. For the first time in nearly a decade, Intel had a real competitor in the consumer processor space. Initially, Intel did not respond to Ryzen’s introduction. After all, when Intel released its 10nm processors in 2018, Ryzen would become obsolete. But Intel failed to do so. What was supposed to be released in 2016 took an additional six years to release. When AMD released its 3rd generation processors in 2020, AMD had surpassed Intel’s final advantage : single-core performance. AMD achieved this with two improvements. First, it implemented its new Zen 2 microarchitecture, and second, it switched from GlobalFoundries to TSMC’s more advanced fabrication.

At the same time Intel struggled with AMD, a new power emerged in the Semiconductors industry. TSMC is a Taiwan-based semiconductor fabrication company. In 2018, TSMC began mass production of its N7 fabrication process. The 7-nanometer process was the most sophisticated fabrication process in the world at the time of its introduction. Intel’s 10nm process was supposed to feature a higher transistor density but did not release on time due to delays. As Intel failed to deliver its 10nm process, TSMC jumped to 5nm in 2020. TSMC was now the undisputed king of advanced semiconductor manufacturing.

One company that recognized Intel’s failure was Apple. From 2005 to 2020, Apple solely used Intel processors in its Mac offerings. However, Apple had utilized Apple-designed TSMC ARM-based architecture processors in its mobile devices since 2014. In 2020, Apple announced that Macs would transition from Intel processors to “Apple Silicon” manufactured by TSMC. This proved wildly successful as Apple’s M1 chip drastically outperformed any of Intel’s mobile processors. Furthermore, Apple’s chips were significantly more efficient than their Intel counterparts due to their usage of an ARM-based architecture. Apple’s success has moved the entire industry. Intel’s once partners have looked into designing their own chips and outsourcing production to companies like TSMC. Intel’s x86 chips could very possibly be replaced by ARM-based chips soon.

Intel’s Response to the Changing Competitive Environment.

When competitive headwinds began hitting Intel in 2017, they did nothing. At the time, its processors were still stronger than the competition. Its CEO, Krzanich, believed that 10nm would give them a competitive advantage over AMD. It is important to note that AMD was on the brink of bankruptcy just a year or two prior to the introduction of Ryzen. When Krzanich left in 2018, the company had never looked financially stronger. Intel doubled its net income from $9.6 billion in 2017 to over $21 billion in 2018. These numbers did not reflect the threat of growing competition from TSMC and AMD.

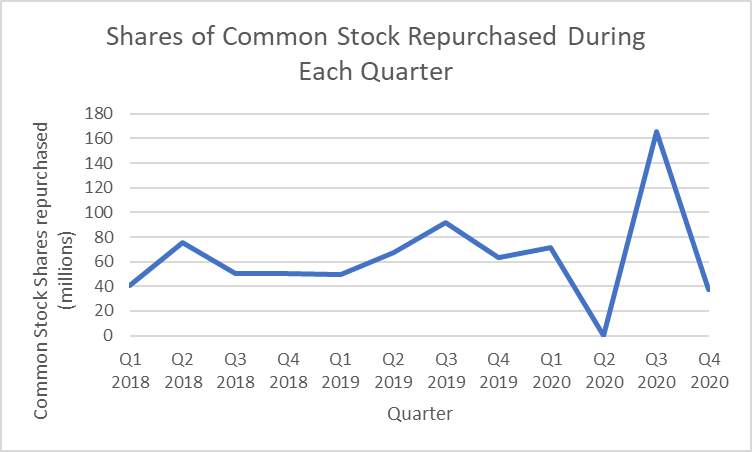

New CEO Swan thought that stock buybacks were appropriate in recognition of the company’s increased profitability. Intel went from buying backing $3.6 billion in shares in 2017 to Buying back $10.7 billion in shares in 2018. This was followed by $13.6 billion and $14.2 billion in 2019 and 2020, respectively. The average share buyback price from Q1 2018 to Q4 2020 was $50.46. The current Intel stock price is $29.00 (43% lower than the $50.46 Swan paid). Swan did not address that 10nm had been delayed for almost four years. He was not able to properly assess the threats facing the firm.

.

Ultimately, the problem was that Intel's financial statements were signaling that the company was in a much stronger position than it was. Management did not see the underlying problems in the business, even though the numbers looked too good to be true. While an investor might be forgiven for making that mistake and buying in at $68, management should have recognized that buybacks do not increase shareholder value when the market has priced in substantial growth that will not be fulfilled due to a decaying competitive position. Bob Swan should have been investing in Intel's core business and expanding into adjacent ones. Considering TSMC's success in manufacturing other companies' chip designs, Intel should have opened a segment dedicated to addressing the same market. Intel could have sold production on its older node processes to companies not needing the most cutting-edge technology. In summary, AMD and TSMC's success could be attributed to Intel's complacency as much as any move either company made.

In early 2021, Patrick Gelsinger replaced Bob Swan as CEO. Gelsinger promised to bring Intel's Engineering culture back to the company and gave it a new vision. Recognizing that the industry was moving toward task-specific processor designs, Gelsinger decided that Intel would begin selling its fab capacity to other companies to build custom chips, putting Intel in direct competition with TSMC. Gelsinger also had Intel rename its node sizes to more accurately line up with their TSMC counterparts. Intel 10nm was renamed Intel 7 because its transistor density was higher than TSMC's 7nm. Intel has announced plans to construct multiple new fabs worldwide, with the most notable being in Ohio and Germany. Intel has expanded its R&D laboratories around the world, intending to achieve technological superiority by 2025. Gelsinger slashed Intel's repurchases of common stock. Most importantly, in 2022, Intel finally released its 10nm processors, six years after their first planned release.

More Setbacks

In March 2021, Pat Gelsinger announced Intel's new IDM 2.0 strategy. This strategy places a significant emphasis on technological superiority and engineering, areas where Intel has struggled in recent years. IDM 2.0 involves Intel mass-producing other companies' designs at its foundries, a model that closely mirrors TSMC's. However, implementing this strategy poses a significant challenge due to the incredible amount of resources required to invest in fabs. For instance, capital expenditures were $24.8 billion and $18.7 billion in 2021 and 2022, respectively, compared to only $14.3 billion in 2020.

In early 2022, Intel announced that it would be spinning off Mobileye into an IPO. Mobileye is the autonomous driving technology segment of Intel. Intel believes that Mobileye could be a major source of growth in the future. However, it is unclear why Intel would be so keen to give away equity in it. Intel paid out $5.6 billion annually to shareholders through dividends. If management believes that Mobileye is such a tremendous value-producing asset, would it not be an intelligent decision to use the capital allocated to dividends to invest in the asset? If management does not believe that Mobileye will succeed under Intel, what does that say about Intel's management?

Furthermore, in 2022, capital was tight. It was unlikely that Intel would receive an optimistic IPO valuation. Mobileye IPO’d at a valuation of $17 billion dollars, far below Intel’s original expectations

In February of 2023, Intel finally announced that it would be cutting its dividend by roughly 66%. Why this move took over two years into Pat Gelsinger’s tenure to happen is still unclear.

Conclusion

Intel's business model was considered outdated, and its management hindered the company's progress. For many years, Intel had to allocate its research and development (R&D) budget between its design and fab business. However, as smaller and more specialized firms entered the market, they were able to compete by focusing their R&D spending in one area instead of spreading it out like Intel. For instance, TSMC and AMD do not have to worry about both design and fabs because they rely on each other's expertise. Meanwhile, Intel had to spend a lot of money on its own fabs without the benefits of using third-party fabs.

In conclusion, Intel's management has destroyed much value over the last four years. However, this does not mean that Intel is a failing company. Intel is still one of the most prominent players in the semiconductor industry, and with management's new focus, a turnaround is not out of the realm of possibility.